One of the most common questions I’m asked as a financial adviser is “will I have enough to have financial security?” It truly is the million-dollar question!

With so many variables involved, there is no set answer, but these days with so many of us expecting to live longer, at least one million dollars is the minimum required to fund a comfortable retirement.

The reason that this figure has become accepted by most experts is this: if you have $1,000,000 making you 5% (after fees) you have $50,000 per year. This may not sound like enough to live on, however is one pillar of your financial independence. If you have your dream home paid off, your super funds pumping & an emergency reserve as well, you will have achieved financial bliss!

This might come as a shock to many, and a lot of people might think that figure is only achievable by winning the lottery, but I can assure you that it is achievable. It requires the right structure, plan and commitment… and a little bit of magic called compounding.

Here’s an example on how you could be on your way to a million dollars, starting with just $5,000. The more you begin with the better, and the earlier you start the more time for the magic of compounding to take effect!

Start with your focus. For this example it’s reaching your goal of one million dollars and become a millionaire.

- Frequency – Regular deposits are recommended straight from your pay. What you don’t see you don’t miss. Setting up the right banking structures is crucial for this. You can automate your accounts so your investment grows without you needing to worry!

- Amount – A minimum 10% of monthly net income is recommended. If that is too high, start smaller and build up. Increase the amount everytime you get a pay rise, so you won’t feel like you are sacrificing as much.

- Rate – Choose investments that suit your risk profile (for example, are you comfortable being a ‘growth’ investor or more ‘moderate’?). In this example, we’ll look at achieving at least a 6-8% annual rate of return.

- Risk (Volatility) – Speaking of risk, remember, high returns generally mean high risk. On the other hand, lower risk means lower returns. So while it may take you longer to get there, it will generally be a smoother ride along the way. Everyone has a different risk tolerance which depends on age, personality, and circumstances.

- Type of investments – High interest savings account to get started, then perhaps managed funds once you have saved enough for the minimum investment. As your balance grows, as a financial adviser we can look at other assets to spread or diversify your investment risk. If you’re taking advantage of the low tax applied to super, in addition to the superannuation guarantee, you may want to salary sacrifice to your super fund – as long as you don’t exceed the concessional contributions cap.

- Age – Obviously it’s best to begin as early as possible, but you can still save a substantial amount whilst you are generating a positive cash flow, by earning more than you spend! If you want to achieve the goal of being a millionaire sooner, you will need a mix of higher contributions and/or higher returns.

- Planning, for emergencies and life events. – We recommend you always have a buffer aside in case of financial emergencies, such as a sudden loss of your job. That doesn’t mean you miss out on enjoyable lifestyle events such as buying a car or going on holiday. Part of our role as your financial planner is to help you understand the impact of these lifestyle choices on your financial position and to plan for them. Remember, living your life today is an important part of your savings and investment plan.

- Goal – The figures quoted here are based upon a $1 million target, however, depending on your lifestyle and expectations, you can revise that amount to suit your circumstances.

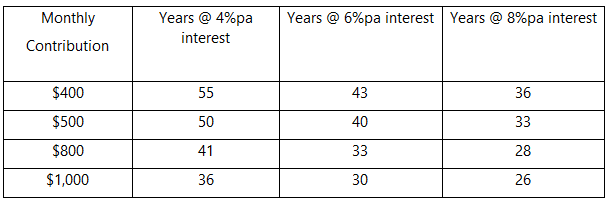

How many years to save $1 million

Let’s start with a savings balance of $5,000. The table below gives you an idea of how much you will need to save and at what interest rate it will need to be invested to achieve that million dollar mark.

Obviously, the earlier you start saving, the smaller the monthly contribution is needed. You can accelerate your contribution rate as your income increases. Savvy savers who pay a mortgage off early can accelerate their program considerably by directing the amount formerly devoted to the mortgage payment into savings.

And what about the money you receive along the way? If you receive an inheritance of say, $100,000 (assuming an annual return of 6%), the $1 million mark can be reached in just 30 years by also contributing only $400 per month.

Regular investing is likened to building a “saving muscle.” You grow accustomed to putting away this money over the years and can increase the amount as you would increase an exercise regimen. Eventually, it becomes a habit, and the payoff can be enormous in the end. Like achieving a fit and healthy body, building your saving muscle results in a healthy financial outlook.

And the best part: once you set this up it goes onto auto-pilot & you can continue on with your life! We have many members that have this set up, and it is just the beginning . When you add your home or a property, plus your superannuation funds into the mix (and make sure everything is in sync with your plans) you will see your wealth skyrocket!

Being a millionaire may seem like an unattainable dream, but with the right amount of planning and action, you can join the Millionaires’ Club sooner than you think.

Note: Taxation and inflation have not been taken into account in these calculations. Calculation is based on achieving $1 million in today’s dollars.